Discover the key takeaways from the Spring Statement 2026 and what they mean for UK businesses, sole traders, and company directors. Learn how to respond to policy changes, strengthen financial planning, and prepare for evolving compliance requirements.

Menu

Close

- Who We Help

Contractors and Freelancers

Clear accounting and IR35 support with straightforward monthly pricing from £95.00 per month

Limited Companies

Complete company accounts, tax, and ongoing support with fixed monthly pricing from £95.00 per month

Sole Traders

Simple accounting and tax support to keep your records organised from £40.00 per month

Construction Industry

CIS tax returns handled accurately and submitted on time from £270 per month

Landlords

Rental income tracking and tax reporting with clear monthly support from £33.00 per month

New startups

Start your business with free company formation and ongoing accounting support

We provide a range of services to accomodate most businesses – check out here - Our Features

MTD compliance

Stay compliant with Making Tax Digital and avoid last-minute issues with clear, ongoing support

Self Assessment

Get your self assessment tax return completed accurately and on time without the usual stress

How to switch to us

Switch accountant without disruption. We handle the full process so nothing is missed

We provide a range of services to accomodate most businesses – check out here

We provide a range of services to accomodate most businesses – check out here - Pricing

- Knowledge

Articles & News

Clear, practical articles on accounting, tax updates, and business topics without unnecessary jargonStep-by-step guides to help you manage your business, stay compliant, and make better financial decisionsWe provide a range of services to accomodate most businesses – check out here - Contact

- Who We Help

Contractors and Freelancers

Clear accounting and IR35 support with straightforward monthly pricing from £95.00 per month

Limited Companies

Complete company accounts, tax, and ongoing support with fixed monthly pricing from £95.00 per month

Sole Traders

Simple accounting and tax support to keep your records organised from £40.00 per month

Construction Industry

CIS tax returns handled accurately and submitted on time from £270 per month

Landlords

Rental income tracking and tax reporting with clear monthly support from £33.00 per month

New startups

Start your business with free company formation and ongoing accounting support

We provide a range of services to accomodate most businesses – check out here - Our Features

MTD compliance

Stay compliant with Making Tax Digital and avoid last-minute issues with clear, ongoing support

Self Assessment

Get your self assessment tax return completed accurately and on time without the usual stress

How to switch to us

Switch accountant without disruption. We handle the full process so nothing is missed

We provide a range of services to accomodate most businesses – check out here - Pricing

- Knowledge

Articles & News

Clear, practical articles on accounting, tax updates, and business topics without unnecessary jargonStep-by-step guides to help you manage your business, stay compliant, and make better financial decisionsWe provide a range of services to accomodate most businesses – check out here - Contact

Completing Your Self Assessment Tax Return in 2026 | UK Tax Guide

June 5, 2026

|

akson

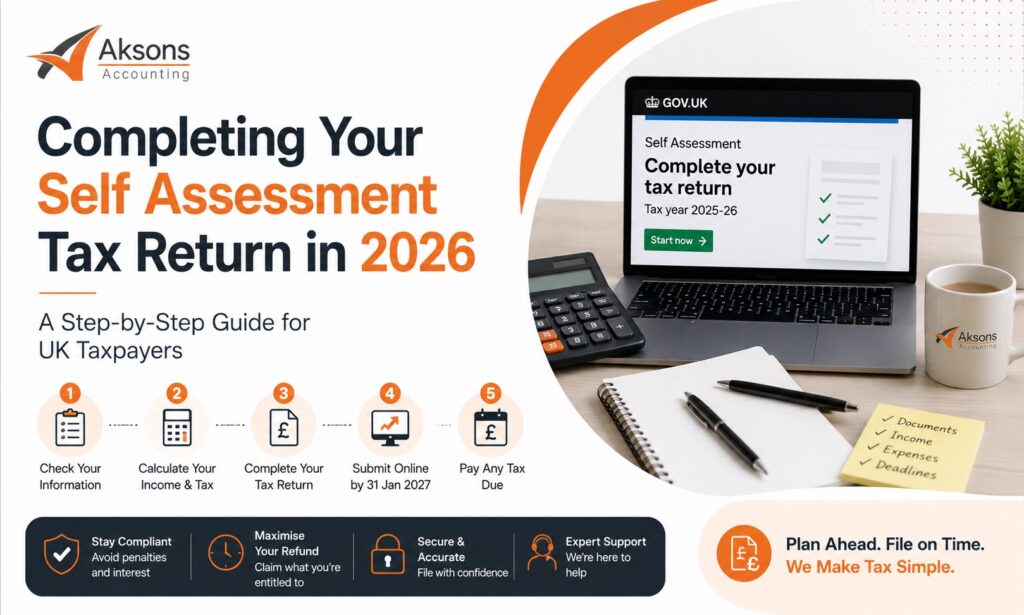

Completing Your Self Assessment Tax Return in 2026

The UK Tax Guide for Sole Traders, Freelancers, Landlords, and Small Business Owners

Most people do not struggle with Self Assessment because the form itself is difficult.

They struggle because their finances are disorganised long before they ever log into HMRC.

Missing invoices. Untracked expenses. Multiple income streams. Side income forgotten until January. Bank statements mixed with personal spending. Pension contributions nobody recorded properly.

By the time the filing deadline arrives, the tax return simply exposes operational disorder that already existed underneath.

That is why Self Assessment becomes stressful for many freelancers, landlords, consultants, directors, and sole traders across the UK.

The return is not only a tax form.

It is a yearly audit of how well your financial systems actually functioned.

And in 2026, that matters even more because the UK tax environment is becoming increasingly digital, more automated, and more closely monitored through:

- Making Tax Digital (MTD)

- banking integrations

- digital record requirements

- real time reporting systems

- stronger HMRC data matching

Businesses and individuals still treating Self Assessment as last minute paperwork are entering a much stricter compliance environment than they did historically.

This guide explains how to complete your Self Assessment tax return properly in 2026, who needs to file common mistakes that trigger penalties, how payments on account work, and what operational habits reduce stress long term.

What Is Self Assessment?

Self Assessment is the system HMRC uses to collect Income Tax from individuals whose income is not automatically taxed through PAYE.

Instead of tax being deducted automatically, individuals calculate and report their income manually through an annual tax return.

The system applies to:

- sole traders

- freelancers

- landlords

- company directors

- contractors

- investors

- high earners

- people with untaxed income streams

HMRC uses the submitted information to calculate:

- income tax

- Class 2 NICs

- Class 4 NICs

- Capital Gains Tax where applicable

Many people assume Self Assessment only applies to self employed individuals.

That is no longer accurate.

Modern income structures became more fragmented:

- side businesses

- digital income

- online selling

- property income

- investments

- overseas earnings

- creator economy revenue

That means more people now fall into Self Assessment obligations than they realise.

Who Needs to Complete a Self Assessment Tax Return?

You may need to file a Self Assessment return if you:

- are self employed

- earned over £1,000 from self employment

- received rental income

- earned untaxed foreign income

- received significant dividends

- sold taxable assets

- earned substantial investment income

- became a company director

- received income outside PAYE

According to UK tax guidance, millions of taxpayers file Self Assessment returns annually, with late filing penalties applying automatically once deadlines pass.

One of the biggest mistakes people make is assuming HMRC will always notify them.

HMRC expects taxpayers to determine whether they need to register themselves.

That distinction matters.

Self Assessment Deadlines in 2026

The UK Self Assessment calendar remains strict.

Key Deadlines

Deadline | Requirement |

5 October | Register for Self Assessment |

31 October | Paper tax return deadline |

31 January | Online filing deadline |

31 January | Tax payment deadline |

31 July | Second payment on account deadline |

The online filing deadline remains the most important date for most taxpayers.

Missing it triggers an automatic £100 late filing penalty even if no tax is owed.

Penalties then escalate over time:

- daily penalties

- interest charges

- additional percentage based fines

The operational issue is rarely the form itself.

It is leaving preparation too late.

What Documents Do You Need Before Starting?

Most Self Assessment stress comes from poor preparation.

Before filing, gather:

- UTR number

- National Insurance number

- P60s or P45s

- self employment income records

- expense records

- dividend statements

- rental income records

- pension contribution records

- charitable donation records

- bank interest information

The businesses and individuals filing smoothly usually maintain records throughout the year.

The ones struggling in January usually reconstruct an entire financial year retroactively.

That difference matters more than tax software itself.

Registering for Self Assessment

If filing for the first time, you must register with HMRC before submitting a return.

Most self employed individuals register online and receive:

- a Unique Taxpayer Reference (UTR)

- login credentials

- activation details

The process itself is straightforward.

The operational mistake is waiting too long.

HMRC activation codes can take time to arrive, especially during peak filing periods.

Every January, thousands of people discover this too late.

Completing the Self Assessment Tax Return

Step 1: Report Employment Income

If employed during the tax year, include:

- PAYE salary

- bonuses

- benefits

- tax deducted

This information typically comes from your P60 or P45.

Step 2: Report Self Employment Income

This section causes the most difficulty for sole traders and freelancers.

You must report:

- total business income

- allowable expenses

- profit calculations

Allowable expenses may include:

- office costs

- software

- professional subscriptions

- travel

- insurance

- phone costs

- marketing expenses

The issue is not claiming expenses aggressively.

The issue is claiming them accurately.

Poor bookkeeping creates:

- underclaimed deductions

- unsupported expense claims

- inconsistent reporting

- audit exposure

Why Expense Tracking Matters More Than People Think

Many sole traders underestimate how much money they lose through weak expense tracking.

Small recurring costs accumulate significantly:

- subscriptions

- mileage

- software

- equipment

- internet usage

- professional tools

Without structured tracking, legitimate deductions disappear.

The opposite risk also exists.

Some individuals attempt to classify personal spending as business expenses without clear justification.

That creates unnecessary compliance exposure.

The strongest approach is operational clarity.

Not aggressive interpretation.

Rental Income Reporting

Landlords must generally report:

- rental income

- allowable property expenses

- mortgage related costs where applicable

- maintenance expenses

Many landlords still underestimate the record keeping requirements involved.

Especially those managing:

- multiple properties

- short term lets

- overseas property income

- jointly owned assets

As digital tax systems expand further through Making Tax Digital reforms, record quality is becoming increasingly important.

Dividend Income and Director Responsibilities

Company directors often underestimate Self Assessment obligations.

Receiving dividends typically creates reporting responsibilities even when PAYE salary already exists.

This becomes especially important for:

- small limited company owners

- agency directors

- consultants operating through companies

Weak separation between:

- personal spending

- director loans

- dividends

- salary

…creates accounting confusion quickly.

At Aksons Accounting Services Ltd, one recurring issue seen across growing SMEs and sole traders is operational growth happening faster than financial structure. Businesses generate more revenue, more transactions, and more payment streams over time while bookkeeping systems remain based on how the business operated years earlier.

That gap usually surfaces during tax season.

Payments on Account Explained

Payments on account confuse many taxpayers every year.

If your tax bill exceeds certain thresholds, HMRC may require advance payments toward the following tax year.

According to UK tax guidance, payments on account are typically due:

- 31 January

- 31 July

Many taxpayers panic because they believe they are being taxed twice.

They are not.

HMRC is effectively collecting future tax earlier based on prior year earnings.

This creates cash flow pressure for:

- freelancers

- consultants

- seasonal businesses

- rapidly growing businesses

Especially when no forecasting exists.

Common Self Assessment Mistakes

Leaving Filing Until January

This creates:

- rushed decisions

- calculation errors

- missing records

- unnecessary stress

Businesses with stable financial operations rarely file at the last moment.

Mixing Personal and Business Spending

This creates bookkeeping confusion quickly.

Especially for sole traders using personal accounts operationally.

Ignoring Side Income

Digital income streams are increasingly traceable.

That includes:

- affiliate revenue

- marketplace income

- creator income

- freelance platforms

- online selling

HMRC visibility continues increasing.

Poor Record Keeping

Weak records create:

- underclaimed expenses

- inaccurate filings

- compliance exposure

- higher accountant costs

The return itself is usually not the root problem.

The bookkeeping is.

Misunderstanding Allowable Expenses

Some taxpayers become overly aggressive.

Others claim almost nothing.

Both approaches create inefficiency.

Making Tax Digital (MTD) and the Future of Self Assessment

Making Tax Digital is changing how self employed taxpayers interact with HMRC.

From April 2026, MTD requirements began expanding for qualifying self employed individuals and landlords above specific income thresholds.

This shift moves businesses toward:

- digital records

- quarterly submissions

- software based reporting

- reduced manual filing

The direction is clear.

HMRC wants:

- less paper

- more automation

- greater visibility

- fewer undeclared discrepancies

Businesses still operating entirely manually will eventually face increasing pressure to modernise systems.

What Happens If You File Late?

Late filing triggers:

- automatic penalties

- daily fines

- interest charges

- escalating enforcement

The initial £100 penalty applies even where no tax is owed.

Longer delays increase financial exposure significantly.

Persistent non compliance can also affect:

- mortgage applications

- lending reviews

- financial credibility

Especially for self employed individuals.

Practical Self Assessment Checklist

Before Filing

- Gather income records

- Organise expenses

- Download bank statements

- confirm dividend records

- review pension contributions

During Filing

- Check figures carefully

- review allowable expenses

- confirm tax calculations

- save submission receipts

After Filing

- Set aside tax reserves

- prepare for payments on account

- review bookkeeping systems

- improve record tracking for next year

Most filing stress comes from operational habits repeated across the year.

Not the return itself.

Practical Self Assessment Checklist

What is Self Assessment?

Self Assessment is HMRC’s system for collecting tax from individuals with income not automatically taxed through PAYE.

Who needs to complete a Self Assessment tax return?

You may need to file if you:

- are self employed

- receive rental income

- earn untaxed income

- receive dividends

- have significant investment income

What is the deadline for online Self Assessment filing?

The online filing deadline is 31 January each year.

What happens if I file late?

Late filing triggers automatic penalties, interest, and escalating fines.

What are payments on account?

Payments on account are advance tax payments toward the following tax year based on your previous tax bill.

Can I amend a submitted tax return?

Yes. HMRC generally allows amendments after submission within specific time limits.

Do sole traders need separate business bank accounts?

Not legally in all cases, but separating business and personal finances significantly improves bookkeeping clarity.

What expenses can self employed individuals claim?

Allowable expenses may include:

- software

- office costs

- travel

- insurance

- marketing

- professional subscriptions

What is Making Tax Digital (MTD)?

MTD is HMRC’s move toward digital tax reporting and software based submissions.

Can HMRC investigate Self Assessment returns?

Yes. HMRC can review returns and request supporting evidence where inconsistencies or concerns arise.

Final Thought

Most Self Assessment problems do not begin inside the tax return itself.

They begin months earlier through weak financial organisation.

Poor bookkeeping.

Untracked expenses.

Mixed accounts.

Reactive filing.

No forecasting.

The tax return simply exposes those weaknesses once deadlines arrive.

The individuals handling Self Assessment best in 2026 are usually not the ones working hardest in January.

They are the ones building cleaner operational habits throughout the year.

Related Articles & News

Discover the key takeaways from the Spring Statement 2026 and what they mean for UK businesses, sole traders, and company directors. Learn how to respond to policy changes, strengthen financial planning, and prepare for evolving compliance requirements.

Learn how Making Tax Digital for Income Tax will affect sole traders, freelancers, and landlords. Understand quarterly reporting, compliance requirements, common challenges, and how to prepare before the new HMRC rules take effect.

Learn what the Companies House WebFiling security issue means for UK businesses, the risks of filing fraud, identity verification changes, and the steps directors can take to protect company records and strengthen compliance.

Learn the latest Companies House filing fees in 2026, including confirmation statement costs, late filing penalties, company incorporation fees, and the hidden compliance risks UK businesses often overlook.

Learn the latest Companies House filing fees in 2026, including confirmation statement costs, late filing penalties, company incorporation fees, and the hidden compliance risks UK businesses often overlook.

Learn the key ICO responsibilities for UK businesses in 2026, including ICO registration, GDPR compliance, data breach rules, subject access requests, CCTV obligations, marketing consent, and SME data protection risks.

A 2026 guide to UK average wage trends, including the latest salary figures, minimum wage changes, real pay growth, regional pressure, and what the numbers mean for businesses and workers.

From April 2026, HMRC’s Making Tax Digital rules will begin changing how sole traders and landlords report income tax. For many businesses, this is not just another compliance update. It changes the rhythm of financial management itself.

Choosing between sole trader and limited company status sets the tax you pay, the paperwork you file, and the personal risk you carry. The right answer depends on your profits, your sector, and your appetite for admin.